Is bitcoin really a digital version of gold?

We had an uncomfortable realization this week while reviewing our portfolio insurance allocations.

Both bitcoin and gold recently touched psychological milestones, $100,000 and $4,000 respectively. Both are now pulling back from all-time highs. And both get marketed as “insurance” against monetary debasement. The comparison is everywhere: bitcoin as “digital gold,” gold as “analog bitcoin.”

But something about this equivalence bothered us. So we spent the past few days thinking through what portfolio insurance actually means in practice.

What insurance really insures against

Portfolio insurance isn’t about hedging normal volatility. It’s about extreme scenarios, the kind where financial infrastructure itself becomes fragile.

The 2008 crisis. The 1970s stagflation. Argentina’s currency collapse. These aren’t hypothetical thought experiments for academic papers. They’re historical events where counterparty risk materialized and payment systems broke down.

Gold has served this insurance function for millennia because of fundamental physical properties: it’s scarce, it doesn’t corrode, it has limited industrial uses, and critically, it exists outside the financial system. In a fiat monetary regime where central banks can expand balance sheets at will, an asset with no counterparty dependency has real value.

The recent surge in gold demand from emerging market central banks illustrates this. They’re not just hedging inflation. They’re seeking alternatives to a US dollar system that increasingly attaches political conditions.

The $28 trillion question

The market cap comparison gets cited constantly: gold at roughly $30 trillion, bitcoin at $2 trillion. The bull case flows naturally from these numbers. Both assets should benefit from rising global wealth and rising demand for monetary insurance. But bitcoin has an additional tailwind, it can capture share from gold’s massive installed market cap.

We get the logic. We hold bitcoin at Arkevium. A meaningful portion of the fund is in it.

But here’s where the comparison breaks down completely.

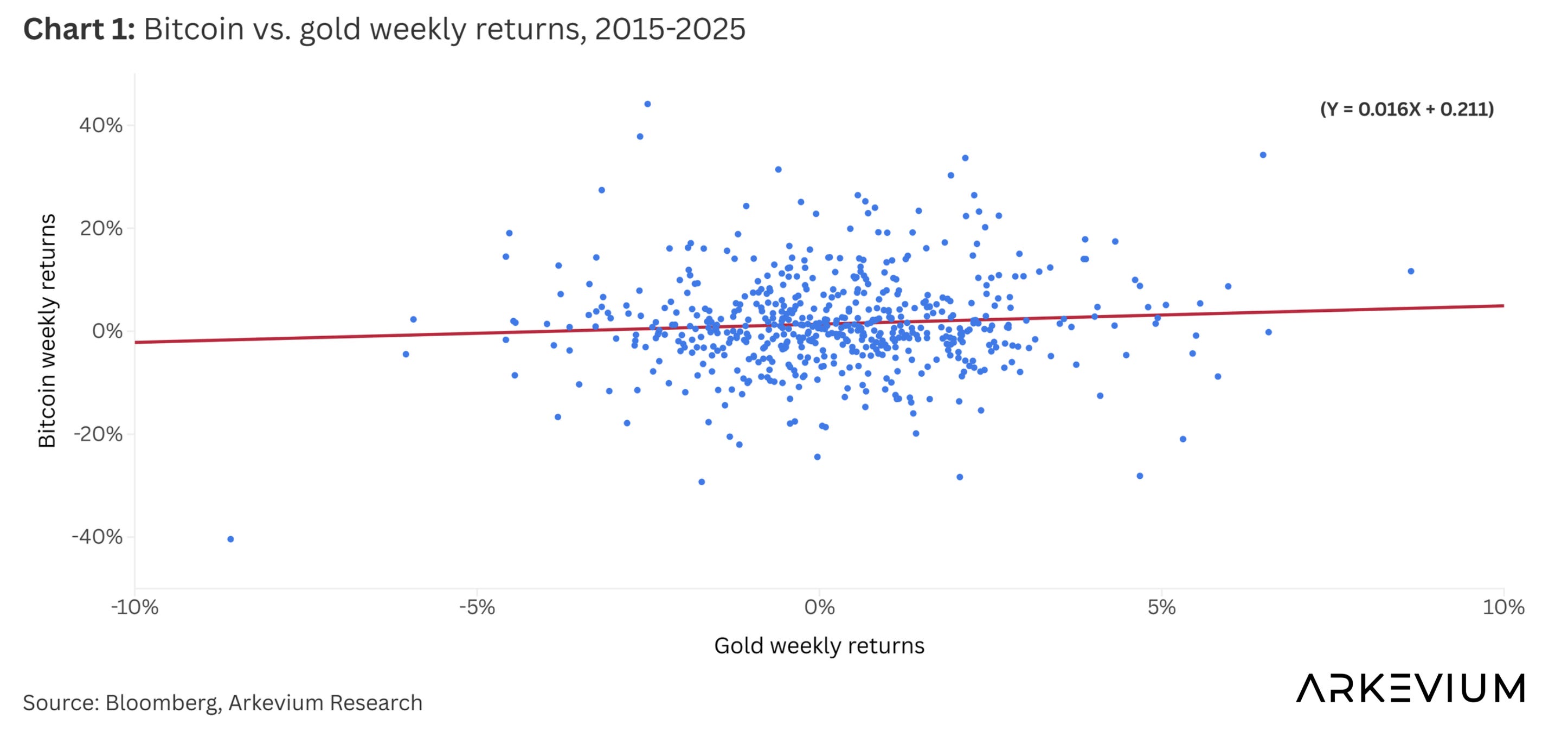

If bitcoin and gold truly served interchangeable portfolio insurance functions, we’d expect their returns to move together. The data suggests otherwise (chart 1).

The physical/digital divide in extremis

Portfolio insurance is specifically about tail scenarios. The scenarios where everything is going wrong simultaneously.

In those moments, we can buy physical gold coins, store them in a safe, and barter them if the banking system fails. This sounds dramatic (perhaps even paranoid) but insurance is precisely about dramatic scenarios. During the 2008 crisis, demand for physical gold spiked as investors questioned whether “paper” gold certificates would actually be redeemable. The physical premium expanded significantly.

Bitcoin offers no equivalent. We cannot hold it physically. We cannot barter it at a local level if payment rails collapse. Yes, the blockchain continues operating. Yes, we can memorize a seed phrase and cross borders. These are valuable properties, but they’re different properties, serving different use cases.

Our point is that in extremis, we’re not sure any digital asset can fulfill the same role as a physical one. The idea that bitcoin and gold are almost interchangeable as portfolio insurance strikes us as fundamentally wrong.

This isn't about bitcoin's technology. It's about what happens when digital infrastructure itself becomes unreliable. In a genuine financial system crisis, the kind where electricity grids are unstable, internet access is restricted, or governments actively interfere with digital transactions, a physical asset has properties that no digital asset can replicate.

The position sizing implication

This distinction has direct consequences for how we think about allocations.

If bitcoin truly serves as equivalent portfolio insurance to gold, then the market cap delta suggests enormous upside. A doubling of bitcoin’s share of the combined “monetary insurance” market would imply substantial appreciation.

But if bitcoin serves a different function, perhaps as a speculative monetary alternative or a hedge against financial censorship rather than systemic collapse, then the comparison is meaningless.

They’re not competing for the same role in portfolios.

We’re not dismissing bitcoin. We think it has genuine value. But we’re skeptical it’s a direct substitute for gold in the insurance role. The physical versus digital distinction isn’t technophobia. It’s a fundamental difference in how these assets function when systems break down.

This is why we treat them as complementary positions rather than interchangeable ones. Gold as insurance against systemic financial failure. Bitcoin as insurance against monetary debasement and financial censorship. Related concerns, but not identical.

Maybe we’re wrong. Maybe the next crisis looks different (more cyber than physical, more infrastructure failure than banking collapse). Maybe bitcoin’s digital properties prove more valuable than gold’s physical ones. We’re genuinely open to that possibility.

But for now, the historical pattern is clear: when financial systems fail, physical assets matter. And that distinction affects how we size these positions.