Can Google break Nvidia's monopoly?

We’ve been long on Alphabet since Q4 2023. It’s the largest position in our AI basket at Arkevium Capital, and last week’s Bloomberg report on Google’s tensor processing units confirmed something we’ve believed for over a year: the AI chip market was always going to fragment.

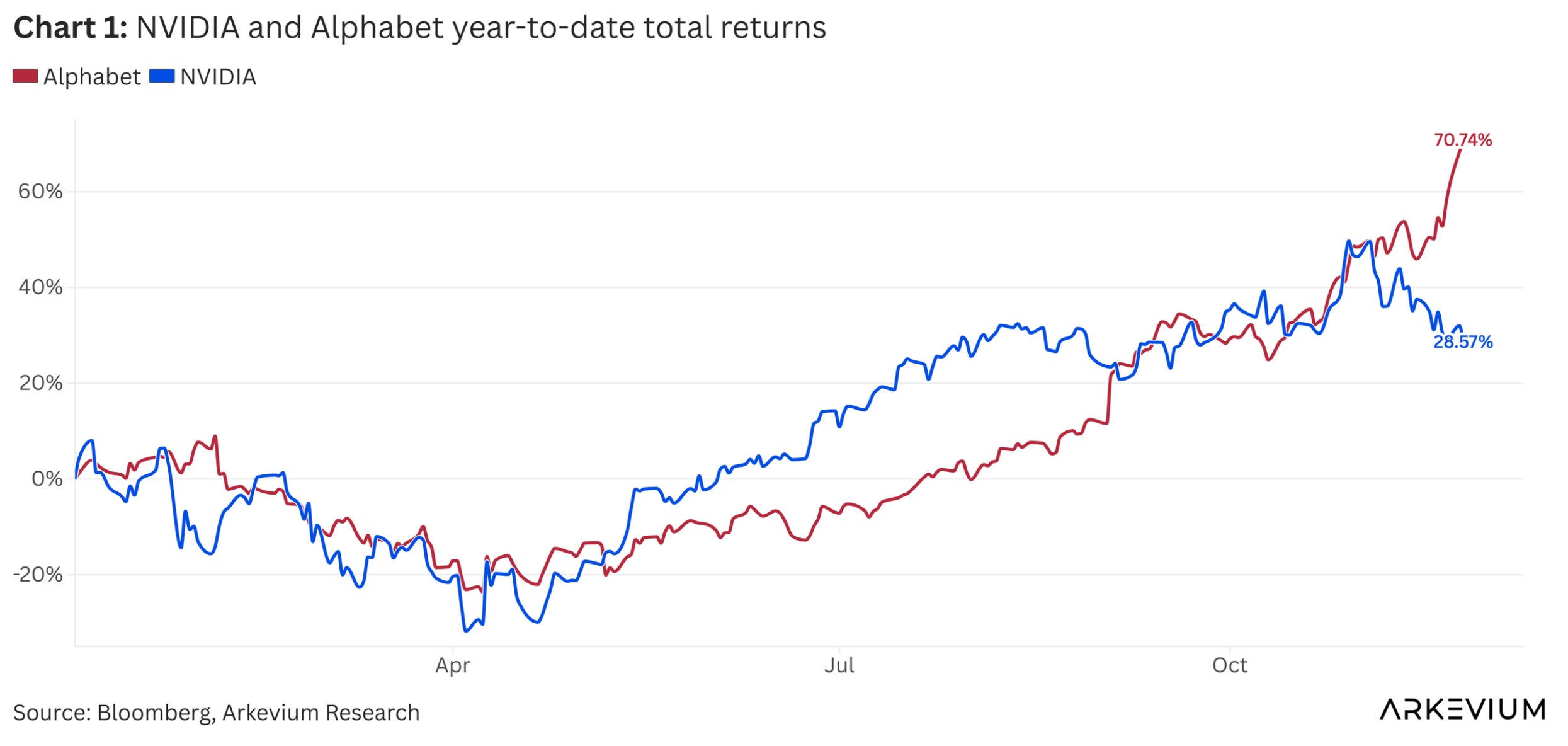

The headline number tells part of the story. Alphabet is up 70.74% YTD. Nvidia, for context, is up 28.57% over the same period (chart 1).

But the more interesting narrative isn’t about relative returns. It’s about what happens when monopolies become vulnerable.

The monopoly paradox

Here’s what we’ve learned watching tech markets for the past decade: monopolies don’t fall because competitors build better products. They fall because the monopolist’s own customers become desperate for alternatives.

Nvidia has owned the AI accelerator market. Their GPUs became the de facto standard. Their CUDA software created switching costs that felt insurmountable. Every major AI lab (Meta, OpenAI, Anthropic) ran on Nvidia infrastructure. Jensen Huang could essentially name his price.

But monopoly pricing creates its own problems. When Nvidia chips become so expensive that cloud providers like Oracle struggle to generate decent gross margins renting them out, something has to give. When your biggest customers are spending tens of billions annually and facing supply constraints, they start looking for alternatives regardless of switching costs. That’s where Google enters the picture.

The TPU strategy

For years, Google has used its tensor processing units internally to train its own models. They’ve also rented TPUs to cloud customers through Google Cloud. But the new development is more aggressive: Google is now pitching companies on using TPUs in their own data centers, not just in Google’s cloud infrastructure.

Meta is reportedly in talks to spend billions on TPUs for deployment in Meta’s own facilities in 2027, plus renting Google chips from Google Cloud in 2026. Given Meta’s projected capex of at least $100 billion for 2026 (with an estimated $40-50 billion allocated to inferencing chip capacity) we’re talking about a material shift in procurement strategy.

This isn’t just about one customer. Google previously secured a deal with Anthropic for up to one million TPUs. Financial institutions and high-frequency trading firms are in discussions about TPU deployments. The pitch is straightforward: TPUs are cheaper than Nvidia chips, and for sensitive data, running them in your own data centers meets higher security and compliance standards.

Some Google Cloud leaders have suggested internally that this strategy could capture as much as 10% of Nvidia’s annual revenue. That’s not a small number. Nvidia’s trailing revenue is in the vicinity of $130 billion annually. Ten percent would represent roughly $13 billion in annual revenue for Google, a meaningful addition to Google Cloud’s existing business.

Why this works now

Timing matters. Three factors have converged to make Google’s TPU push credible.

First, Google’s AI capabilities have legitimately caught up. The Gemini 3 release earlier this month received enthusiastic reviews from prominent tech figures who believe Google has eliminated the gap with OpenAI. You can’t sell AI chips if customers doubt your AI expertise. Google’s recent technical progress gives TPUs credibility they might have lacked two years ago.

Second, developers increasingly believe Google has narrowed Nvidia’s lead in the dense server clusters needed to train large models. Meta isn’t just talking to Google about inference workloads, they’re also discussing using TPUs to train new AI models. If TPUs can handle training, not just inference, the addressable market expands dramatically.

Third, Google has developed software called TPU Command Center to make it easier for developers to work with TPUs. This matters because Nvidia’s biggest moat has always been CUDA, the software layer that AI developers know intimately. If Google can reduce switching friction, price becomes a more decisive factor.

The leverage game

Here’s where it gets interesting from a game theory perspective. Even if Google captures only modest market share, the mere existence of a credible alternative creates leverage for Nvidia’s biggest customers.

Look at what happened after Google’s Anthropic deal became public. Jensen Huang immediately announced a multi-billion dollar investment in Anthropic and secured a commitment from them to use Nvidia GPUs. When OpenAI’s plans to rent Google TPUs leaked, Huang struck a tentative deal to invest up to $100 billion in OpenAI for data center development.

Nvidia is reacting defensively. They’re using their balance sheet to lock in customers. That’s rational behavior when you’re defending a dominant position, but it’s also expensive. And it suggests Nvidia recognizes the competitive threat is real.

From the customer perspective, this dynamic is valuable even if they never fully switch to TPUs.

Having Google as a credible alternative vendor strengthens their negotiating position with Nvidia. It caps how much pricing power Nvidia can exercise. It ensures they have supply optionality if Nvidia faces manufacturing constraints.

What we are watching

The Meta-Google negotiations are the key near-term catalyst. If that deal closes, it validates the entire TPU strategy. Meta is sophisticated. They understand the technical tradeoffs. If they’re willing to commit billions to TPUs for both training and inference, it signals Google has achieved technical parity where it matters.

The longer-term question is whether Google can sustain the engineering investment required to keep TPUs competitive. Nvidia doesn’t stand still. They’re iterating rapidly on new architectures. Google needs to match that pace while simultaneously building the software ecosystem that makes TPU adoption frictionless.

Whether TPUs capture 10%, 15%, or 20% of the accelerator market matters less than the structural change underway. The AI chip market is fragmenting. Monopoly pricing power is eroding. And Google has positioned itself as the primary beneficiary of that transition.

That’s why we are staying long Alphabet. The TPU opportunity alone could drive material upside to Google’s growth trajectory. Combined with their improving AI model performance and entrenched position in search, the risk-reward remains compelling.