When 10% of consumers drive 50% of spending

The narrative of US economic resilience is misleading.

We’ve been analyzing the data, and while headline numbers look robust, the engine driving them is becoming dangerously narrow. We are witnessing the return of the “K-shaped” economy, but this time, the divergence is creating a structural fragility that markets are underpricing.

Economist Peter Atwater calls it a “Jenga tower.” We think that’s the perfect analogy. The structure keeps getting taller, but the base is being pulled out block by block.

Here is our thesis on why the US economy is more top-heavy, and fragile, than it appears.

Structural inequality is now a systemic risk

The divergence between the “haves” and “have-nots” isn’t just a social issue anymore, it’s a macro-critical risk factor.

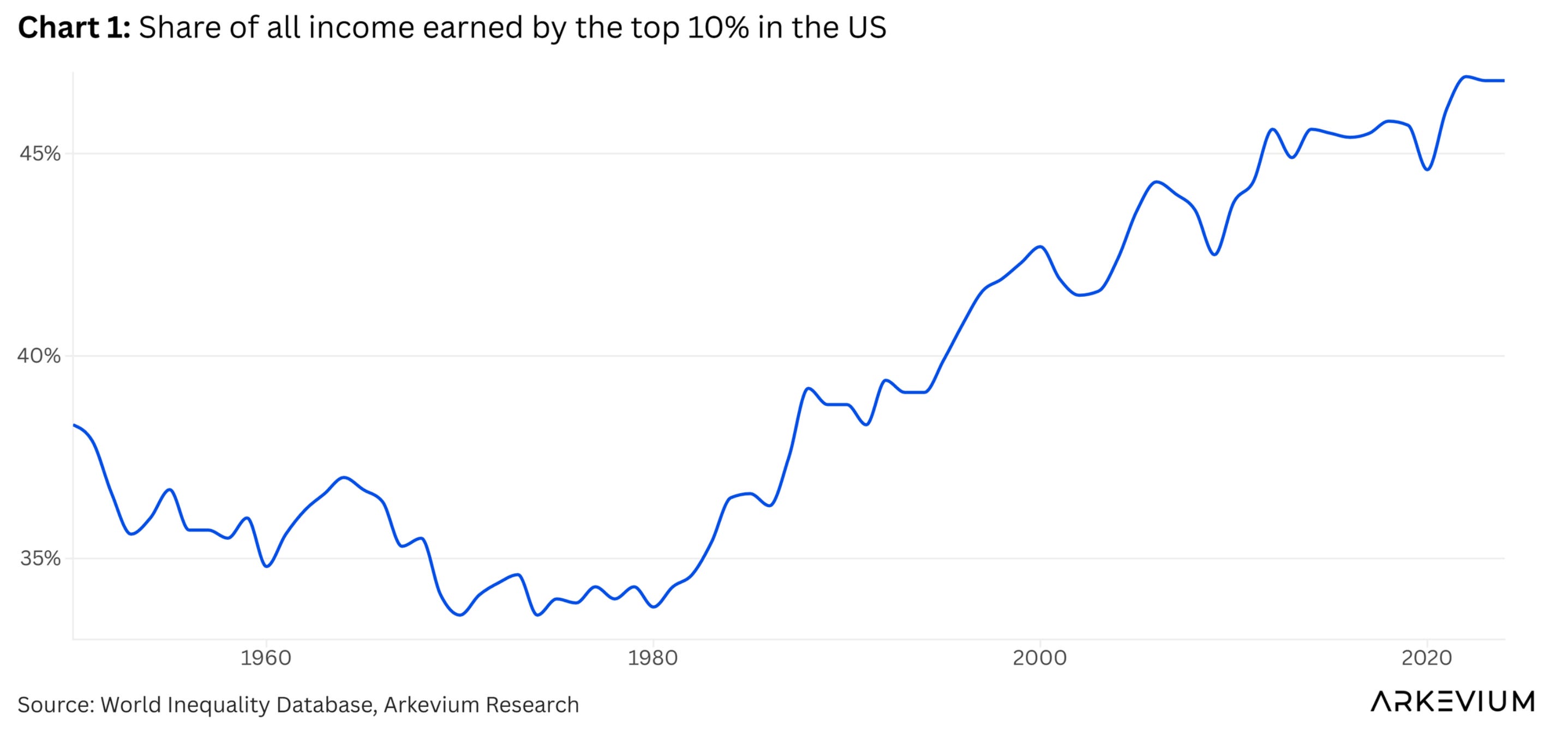

For decades, we have watched the income gap widen. But in the post-pandemic era, this trend has accelerated to unsustainable levels. The top 10% of income earners now capture nearly 50% of all income in the United States (chart 1).

This matters because it dictates who is actually keeping the economy alive.

With inflation eating into purchasing power and the labor market softening, the bottom of the K (the lower and middle income earners) are tapped out. Their wage increases are barely keeping pace with the cost of living.

Meanwhile, the top of the K is experiencing a completely different reality, fueled by asset price inflation in equities and real estate.

The concentration of consumption

Because income is concentrated, spending is concentrated. This is where the risk lies.

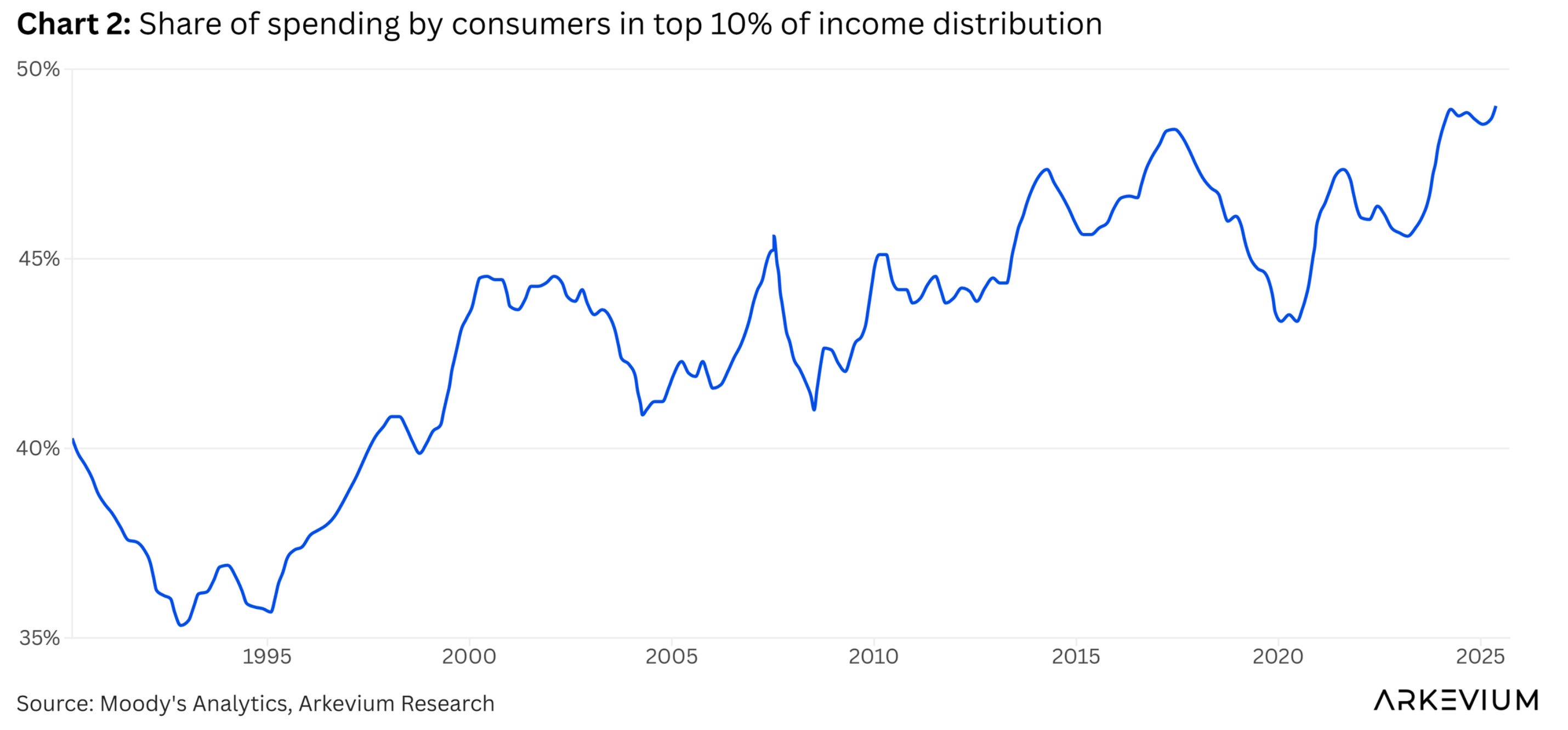

Here, the divergence is even more pronounced. The wealthiest 10% of Americans now account for approximately 50% of all consumer spending (chart 2), a record high. The top 20% control 63% of total consumption. Meanwhile, the bottom 80%, which represented 42% of spending before the pandemic, has been compressed to just 37%.

This chart explains the “mystery” of the resilient economy. The economy hasn’t avoided recession because the average American is doing well. It avoided recession because the top 10% are spending aggressively, buoyed by the wealth effect of record-high stock markets.

But this creates a single point of failure.

If equity markets correct, the “wealth effect” evaporates. The top 10% will pull back. Since the bottom 80% has no capacity to step up and fill the gap, even a moderate drop in asset prices could trigger a sharp, consumer-led recession.

The Fed’s blunt tool is worsening the split

The Federal Reserve is inadvertently exacerbating this bifurcation.

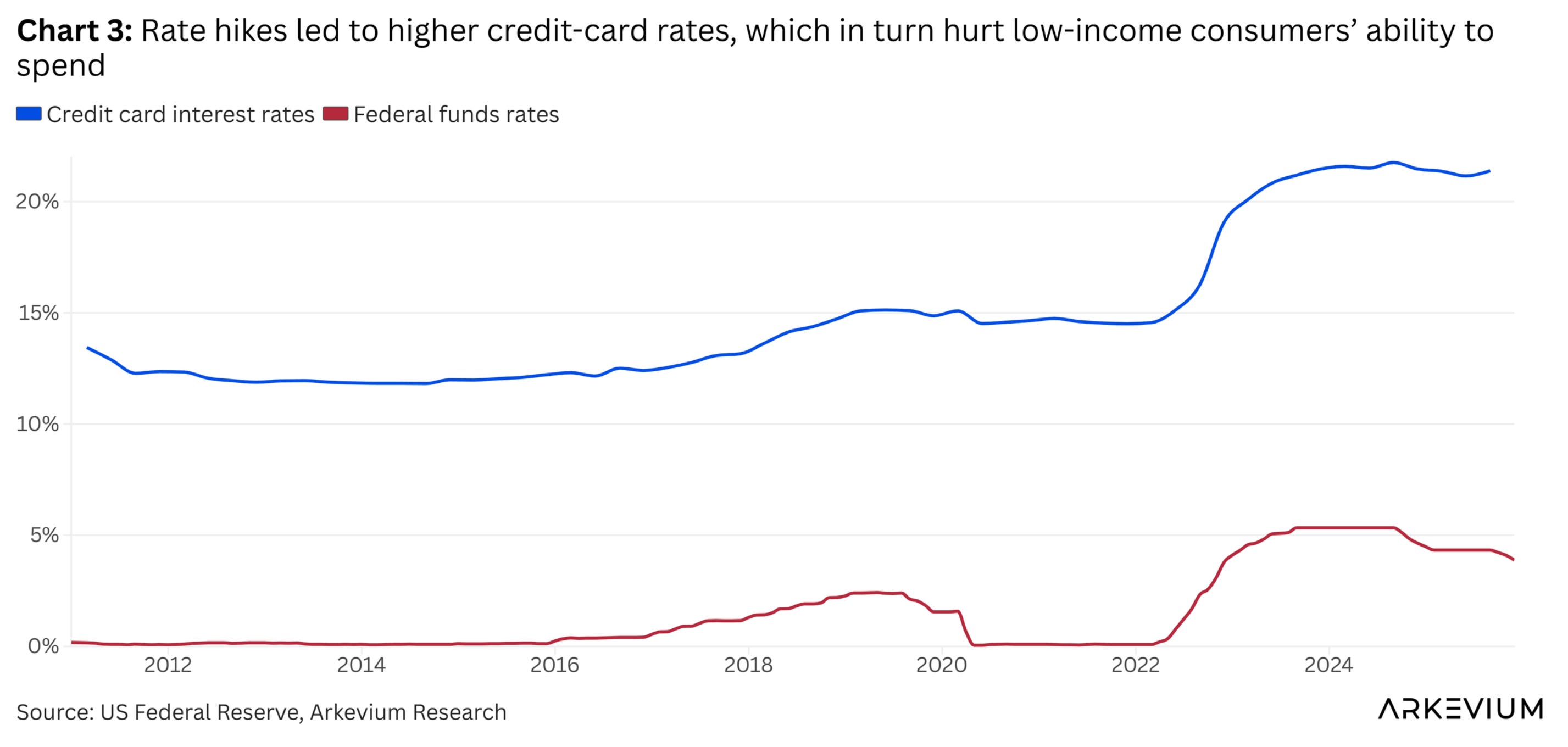

Jerome Powell has admitted that rates are a blunt tool. They cannot target specific demographics. However, restrictive monetary policy is hitting the economy from the bottom up, not the top down.

High interest rates punish borrowers. Low-income consumers rely on credit cards to bridge the gap between wages and inflation. As the Fed hiked rates, credit card interest rates skyrocketed in lockstep.

Investment implications

From a positioning perspective, this analysis suggests several conclusions.

First, equity market stability has become the critical variable for US growth. Monitoring consumer confidence among high-income households matters more than traditional labor market indicators. We’re watching discretionary spending patterns at premium retailers and luxury goods sales as leading indicators.

Second, the wealth effect works both ways. If equities correct 15-20%, we’d expect a sharp, sudden shift in consumption patterns, not a gradual adjustment. Portfolio construction should account for this tail risk through either defensive positioning or explicit hedges.

Third, this environment favors businesses with pricing power and market positions insulated from mass-market consumer weakness. Companies relying on broad-based consumer demand face structural headwinds.

The policy response options are limited. The Fed’s toolkit can’t address this bifurcation. Fiscal policy could theoretically redistribute income or support lower-income consumers, but the political will seems absent. That leaves markets vulnerable to the whims of wealthy households’ spending decisions.

We’re not predicting imminent recession. But we are arguing that the US economy’s stability rests on a narrower foundation than the headline data suggests. The “Jenga tower” stands tall, for now. But the blocks supporting it are fewer than they appear, and the consequences of removing the wrong one have never been greater.